Market Update & Salary Survey – July ’23

Snapshot data on the Management/Executive jobs market as we hit the mid-way point in 2023 shows very slightly slowing and subdued activity, but taken into context, this is primarily just reflective of the dramatically heightened demand seen immediately after the pandemic and the knock-on effect of reduced candidate supply.

The reality is that even with the slight drop in overall job vacancies and the similarly slight increase in candidate supply, there still exists a supply challenge, demonstrated by the continued increase in salaries being offered/demanded in the last 12 months.

Overall, candidate supply is challenging though, especially with the supply of ‘top drawer’ candidates where, if anything, it has slightly reduced due to dampened enthusiasm in response to current economic uncertainty. Attracting ultimate high-quality candidates is still the biggest challenge and threat to businesses.

The broader employment market shows similar trends, June’s ONS data:

- Record number of people in employment, 76%, (up 0.2% on previous quarter)

- No. of payrolled employees increased 23,000 on prior month, up to record high of 30.0m

- Workforce Jobs (including Self-Employed) also all-time record at 36.8m, over 500,000 increase in H1

- 2,031,000 live job vacancies [Source: REC Labour Market Tracker] – more vacancies than active jobseekers, 1,303,000

- Unemployment rate announced today (July 11th) at 4.0%

Focusing again on management/leadership grade recruitment, the overall UK volumes are down very slightly (new instructions and appointments), however, those figures are significantly skewed by the drop in activity and placements in London & the South-East.

The KPMG UK Report on Jobs shows the steepest rise in ‘permanent labour supply’ for 2 years, but does highlight that almost all of that increase is centred in London and surrounding areas where the KPMG reports cites:

‘Rapid contraction in permanent placements’ as ‘employers take an increasingly cautious approach to recruitment as economic uncertainty plays out, especially within the finance sector’.

KPMG Report On Job 2023

The North, and even more so the North-West has conversely seen a notable increase in activity in both new role instructions and placements – my own experience/activity as well as industry figures – with increases in both metrics in 5 of the first 6 months of this year, compared to even the heightened levels of 2022.

This all leads to a market that remains challenging to attract key talent, especially in the North-West.

Financial, Service and Leisure sectors have seen the greatest increase in demand for candidates, Manufacturing has held roughly steady with a modest increase; Retail, IT & Construction seeing the most notable decrease.

The key to successful attraction is searching out of sector. 62% of placements this year have been from a different sector compared to 54% last year and a historic 41% over the pre-covid marketplace.

The impact of candidate scarcity can also be seen in the breakdown of our searches this year.

The average number of target approaches (headhunts) for each search has increased almost 50% with an average of 15 per first (client) interview compared to 11 per interview during 2022, that worsens to offers with the average number of (client) interviewed candidates for each placed role increasing from 4 to 6 giving us almost 100 headhunt approaches per job assignment/offer. We have still maintained a 100% successful completion on retained mandates this year, and have likewise upheld our Guaranteed Search product with delivery in 8 weeks.

Salaries

Q1 2023 saw a slight softening of salary increases compared to 2022, with the Permanent Salaries Index (PSI) showing an average increase of 5.8% (7.6% for new appointments – both cost of living challenges and need to attract staff being the prime drivers), but today’s ONS data shows weekly wage increase from March to May rising to 7.3%, the highest level in modern history (albeit expected with rises in the National Minimum Wage and numerous pay reviews hitting figures in April, with Private Sector weekly wage growth growing faster at 7.7%. The North of England has seen the highest increases in salaries with Q1 PSI data showing a 7.8% average increase, expected to increase further to reflect on today’s ONS data.

This backs up my own findings on new appointments. Management pay rewards (£60-100k) are seeing the greatest increases with an average salary increase for new appointments being very slightly below 10%. This softens at Senior Leadership grades above £100k with average increases of just above 5%.

Package values are strengthening slightly ahead of salaries, again based on new appointments. Bonuses and equity/shares/options/LTIP schemes both seeing a notable increase albeit linked to both personal and business performance. Pensions have likewise seen an increase in employer contributions, but matched with increased employee contributions.

Of equal importance remains employment conditions. Hybrid working, social conscience and employee welfare rank highly in all targeted candidates ‘wish lists’ along with a continually increased prevalence of prospects/job security post-Covid. The majority of targeted candidates ranking those elements as more important than marginal short-term salary increases.

Salary Survey

Salary levels for current employees are still a significant issue for businesses; we conducted a North-West centric salary survey and with a 6,728 sample size taken from Jun 28th to July 3rd, can see notable trends within the current employee base.

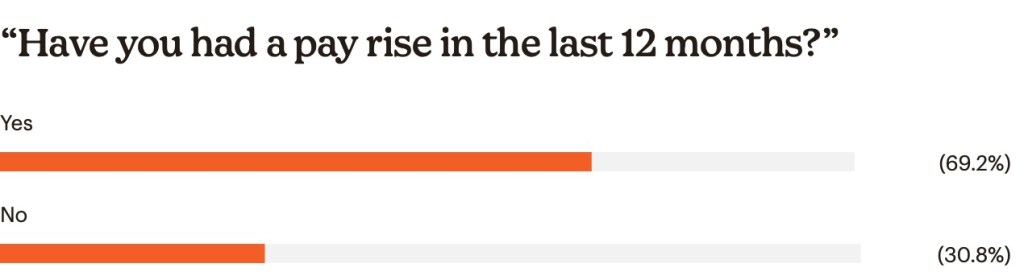

69.2% of respondents have seen pay rise this year, almost double the levels seen in 2011.

Payrise levels vary tremendously. The average pay increase was 5.8% (reflecting the PSI stats), with almost a fifth of people receiving over 10%.

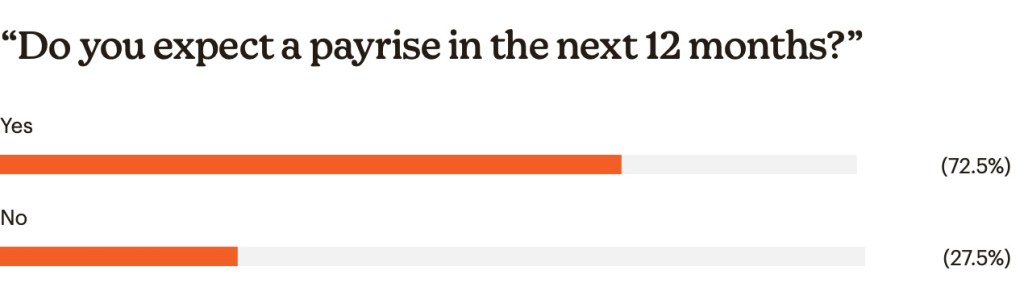

Despite 70% receiving a payrise, over 50% of respondents are dissatisfied with their level of pay….

…..and almost three-quarters expect a rise in the next 12 months

Backing up the above, over 50% say Salary is the most important component (up from 36% last year), Hybrid Working is still the second most important component.

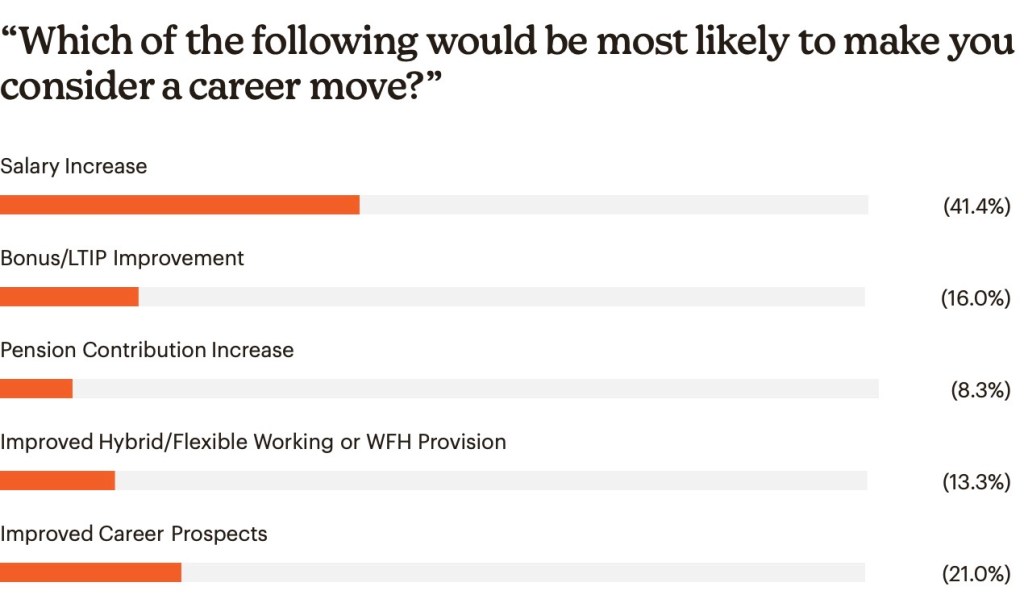

Drivers to cause employees to consider a move are more evenly split. 41% cite Salary, but Career Prospects now sits as the second most common reason, overtaking Hybrid Working and Bonus.

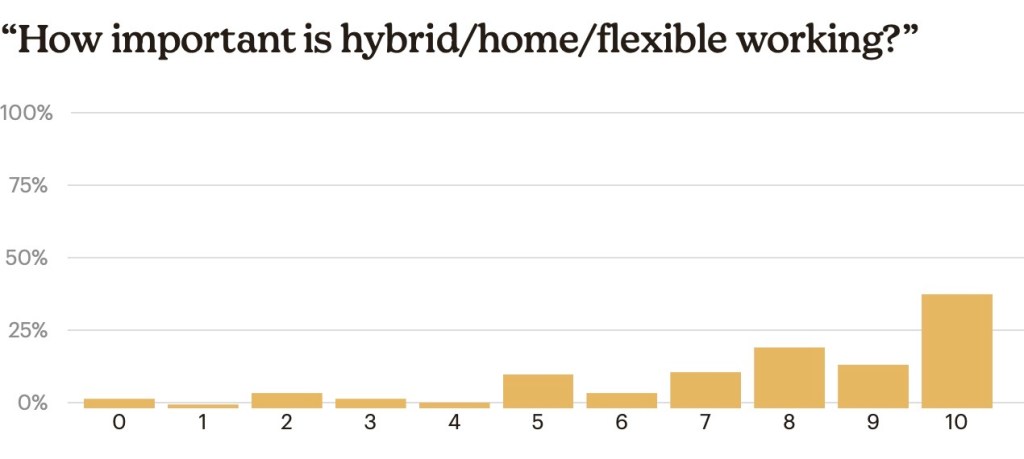

Despite the above, Hybrid Working is still a key component of any package. Only 3% said it was unimportant, 33% calling it very important. The average score was 7.5.

Social Conscience and Ethics of employers has seen a steady increase in importance to employees AND prospective employees – the vast majority of respondents saw it was being important, less than 2% seeing it as unimportant. The average score was 7.8.

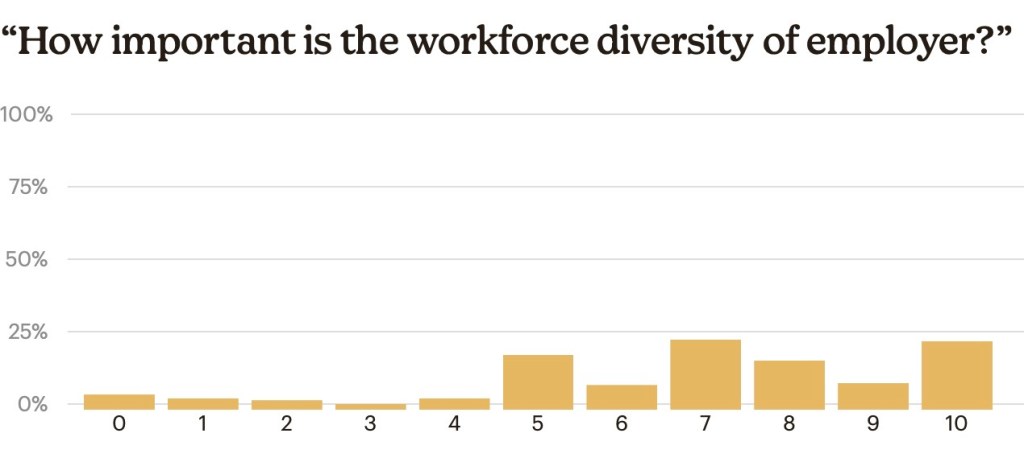

Employer approach to Diversity is also increasingly important with only 4% of people now seeing it as being unimportant, the majority seeing it a being an important part of their employers mindset. The average score was 6.7.

Salary Levels

With the above in mind, salary levels have seen substantial variability over recent months, therefore generically advising on salaries and overall reward packages is even more difficult.

Taking salaries/packages of those we have placed over the past 12 months alongside specific salary benchmarking exercises we have undertaken for clients, leaves me to advise the below as a broad guide for North-West businesses.

| Salary | Bonus | Pension | Healthcare | Notice | ||

| C-Level | £150,000+ | 30-100% | 8-10% | Family | 12mths | |

| Director | £125-£180,000 | 30-50% | 8% | Family | 6-12mths | |

| Leadership | £80-120,000 | 20-40% | 5-8% | Family | 3 mths | |

| Management | £50-85,000 | 15-25% | 4% | Partner | 1 mth | |

| Operational | to £50,000 | – | 4% | Partner | 1 mth | |

Conclusion

The overall Management/Executive recruitment market is holding up despite macroeconomic concerns with continued growth in the North of England more than countering the modest reductions seen in London/the South-East.

REC in their recent survey (June 23) states employer hiring confidence increasing across every sector from Q1 to Q2 this year, Q2 showing an 8% increase in recruitment activity compared to Q1, and as of last month, being even higher than this time last year when job vacancies were at their previous all-time high.

However, the overwhelming majority of employers are still citing significant difficulties in attracting and sourcing the right talent amidst rising costs – forcing them down a path of offering both increased salaries/packages and improved working conditions.

Salaries are continuing to present a significant challenge for employers, today’s data only further increases that pressure, and with salaries increasingly prominent in both importance in current remuneration and motivation to move jobs, that challenge is very real.

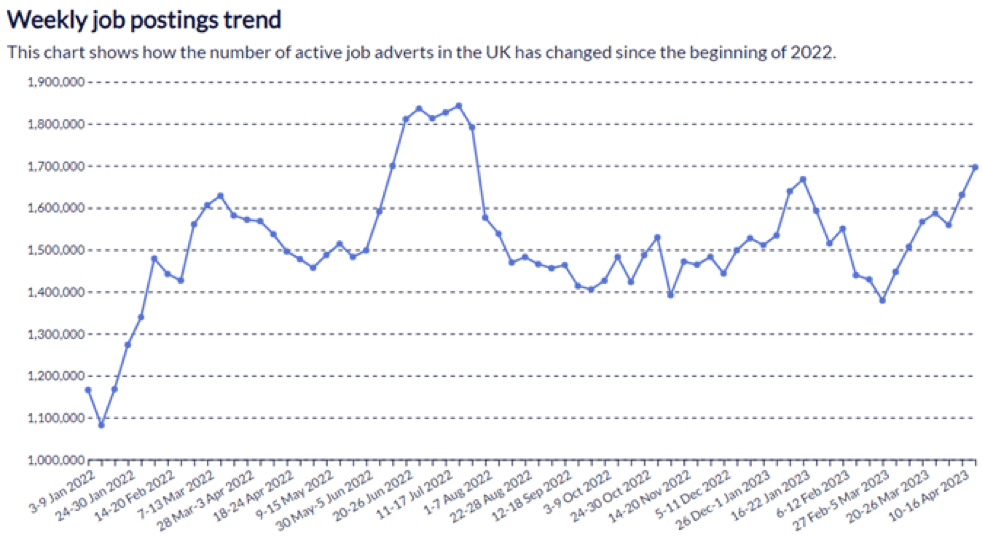

One final note in looking to the remainder of this year: In April, the number of job adverts in the UK stood at 1.7m the highest level for 12 months and the steepest increase since the pandemic (see chart below), That current figure is 2.03m, higher than the peak of the post-Covid spike; the challenges in securing key talent are increasing, not easing.

Currently job postings would literally be off the chart with not only the highest levels, but also the steepest growth.